Comparing Retirement Plans for Small Business Owners

A detailed comparison of various retirement plans to help small business owners choose the best option for their future.

A detailed comparison of various retirement plans to help small business owners choose the best option for their future.

Comparing Retirement Plans for Small Business Owners

Hey there, fellow small business owners! Let's talk about something super important, but often pushed to the back burner: retirement planning. I get it, running a business is a 24/7 gig. You're juggling operations, marketing, sales, and probably a dozen other things. But thinking about your future, and the future of your employees, is crucial. It's not just about saving for your golden years; offering a solid retirement plan can be a huge perk for attracting and retaining top talent, especially in today's competitive market. Plus, there are some sweet tax advantages to be had!

So, you're probably wondering, "Which retirement plan is right for my small business?" That's a fantastic question, and honestly, there's no one-size-fits-all answer. It depends on a bunch of factors: how many employees you have, your budget, how much you want to contribute, and how much administrative hassle you're willing to take on. Don't worry, we're going to break down the most popular options, compare their features, and even recommend some specific providers to make your decision a whole lot easier.

Understanding Retirement Plan Basics for Small Businesses

Before we dive into the nitty-gritty of each plan, let's quickly cover some fundamental concepts. Most retirement plans for small businesses fall into two main categories: defined contribution plans and defined benefit plans. For small businesses, defined contribution plans are far more common and generally simpler to administer. These plans allow you and your employees to contribute a certain amount, and the retirement benefit depends on the investment performance of those contributions. Defined benefit plans, like traditional pensions, promise a specific payout at retirement, but they're much more complex and expensive to manage, so we'll focus primarily on defined contribution options.

Key terms you'll hear a lot are 'employer contributions' (money you put in for your employees), 'employee contributions' (money employees put in from their paychecks), 'vesting' (when employees gain full ownership of employer contributions), and 'fiduciary responsibility' (your legal obligation to act in the best interest of plan participants). Don't let these terms intimidate you; we'll explain them as we go.

SEP IRA Simplified Employee Pension Individual Retirement Arrangement

Let's kick things off with one of the simplest options: the SEP IRA. This plan is a fantastic choice for self-employed individuals and small business owners with no employees, or just a few. It's incredibly easy to set up and administer, making it a popular choice for those who want minimal paperwork.

SEP IRA Key Features and Benefits for Solopreneurs

- Who it's for: Self-employed individuals, sole proprietors, partnerships, and small businesses with few or no employees.

- Contributions: Only employer contributions are allowed. You can contribute up to 25% of an employee's compensation (or 20% of your net earnings from self-employment) up to a maximum of $69,000 for 2024.

- Flexibility: Contributions are discretionary. You don't have to contribute every year, and you can vary the amount you contribute.

- Ease of Administration: Very low administrative burden. No annual IRS filings (like Form 5500) are typically required.

- Tax Advantages: Contributions are tax-deductible for the employer, and earnings grow tax-deferred until retirement.

SEP IRA Use Cases and Scenarios

Imagine you're a freelance graphic designer, a consultant, or a small business owner with just yourself and maybe one or two part-time contractors. A SEP IRA is perfect because it allows you to save a significant amount for retirement with very little fuss. If you have employees, you must contribute the same percentage of compensation for them as you do for yourself. This can be a drawback if you want to contribute a lot for yourself but can't afford to do the same for all your employees.

Recommended SEP IRA Providers and Pricing

Most major brokerage firms offer SEP IRAs. They are generally low-cost, often with no setup or annual maintenance fees, though investment fees will apply depending on what you choose to invest in.

- Fidelity: Offers a wide range of investment options, including commission-free ETFs and mutual funds. No account fees.

- Vanguard: Known for its low-cost index funds and ETFs. No account fees, but minimum investment requirements for some funds.

- Charles Schwab: Similar to Fidelity, offering a broad selection of investments and no account fees.

Pricing: Typically, you'll pay expense ratios on the mutual funds or ETFs you choose, which can range from 0.03% to 1% or more annually. Some providers might charge trading commissions for individual stocks, but many offer commission-free trading for a wide selection of investments.

SIMPLE IRA Savings Incentive Match Plan for Employees Individual Retirement Arrangement

Next up, we have the SIMPLE IRA. This plan is a step up in complexity from the SEP IRA but still relatively straightforward. It's designed for small businesses with 100 or fewer employees and requires both employer and employee contributions, making it a more robust retirement benefit for your team.

SIMPLE IRA Features and Benefits for Growing Businesses

- Who it's for: Small businesses with 100 or fewer employees who earned at least $5,000 in the preceding year.

- Contributions: Both employer and employee contributions are allowed. Employees can contribute up to $16,000 for 2024 ($19,500 if age 50 or older). Employers must either match employee contributions dollar-for-dollar up to 3% of compensation or make a non-elective contribution of 2% of compensation for all eligible employees.

- Vesting: All contributions are immediately 100% vested, meaning employees own the money right away.

- Ease of Administration: More administrative work than a SEP IRA, but less than a 401(k). No annual IRS Form 5500 filing required.

- Tax Advantages: Contributions are tax-deductible for the employer, and employee contributions are pre-tax, reducing their taxable income. Earnings grow tax-deferred.

SIMPLE IRA Use Cases and Scenarios

Let's say you have a small marketing agency with 5-10 employees. You want to offer a retirement plan that encourages your team to save, and you're willing to contribute to their savings. The SIMPLE IRA is a great fit because it mandates employer contributions, which is a strong incentive for employees. The immediate vesting is also a big plus for employee morale and retention.

Recommended SIMPLE IRA Providers and Pricing

Similar to SEP IRAs, many financial institutions offer SIMPLE IRAs. The costs are generally low, primarily consisting of investment fees.

- Fidelity: Offers a straightforward setup process and a wide array of investment choices.

- Vanguard: Excellent for those who prefer low-cost index funds and ETFs.

- Merrill Edge: Provides a good balance of investment options and customer support.

- Guideline: While primarily known for 401(k)s, they also offer SIMPLE IRAs with a focus on low fees and automated administration.

Pricing: Expect similar investment expense ratios as SEP IRAs. Some providers might charge a small annual administrative fee (e.g., $25-$50 per year per account), but many waive these for larger balances or certain investment choices. Guideline, for instance, might have a monthly base fee plus a per-participant fee, but it's generally very competitive for the services offered.

Solo 401k Individual 401k or One Participant 401k

For the self-employed or business owners with no full-time employees other than themselves and their spouse, the Solo 401(k) is a powerhouse. It allows for significantly higher contribution limits than a SEP or SIMPLE IRA, making it an excellent choice for high-income solopreneurs.

Solo 401k Advantages for Self Employed Professionals

- Who it's for: Self-employed individuals, sole proprietors, partnerships, and business owners with no full-time employees (other than a spouse).

- Contributions: You can contribute in two capacities: as an employee and as an employer. As an employee, you can contribute up to $23,000 for 2024 ($30,500 if age 50 or older). As an employer, you can contribute up to 25% of your net earnings from self-employment. The combined total contribution (employee + employer) cannot exceed $69,000 for 2024 ($76,500 if age 50 or older).

- Roth Option: Many Solo 401(k)s offer a Roth option for employee contributions, allowing for tax-free withdrawals in retirement.

- Loan Feature: Some Solo 401(k) plans allow you to borrow from your account, which can be a useful feature for business owners.

- Ease of Administration: Relatively low administrative burden, similar to a SEP IRA, until assets reach $250,000, at which point an annual Form 5500-EZ must be filed.

Solo 401k Use Cases and Scenarios

If you're a successful consultant, a real estate agent, or a small business owner with no employees, and you want to maximize your retirement savings, the Solo 401(k) is probably your best bet. The ability to contribute both as an employee and an employer allows for much higher annual contributions compared to a SEP IRA, especially if your income is substantial.

Recommended Solo 401k Providers and Pricing

While many brokerages offer Solo 401(k)s, some specialize in making them easy to set up and manage, especially for the self-employed.

- Fidelity: Offers a robust platform with diverse investment options and no annual fees for their self-directed Solo 401(k).

- Vanguard: Another strong contender for low-cost index funds and ETFs, with no annual account fees.

- E*TRADE: Provides a user-friendly platform and a wide range of investment choices.

- MySolo401k.net: Specializes in Solo 401(k)s, offering checkbook control and alternative investment options (like real estate) for a one-time setup fee and a small annual fee.

Pricing: For standard brokerage Solo 401(k)s, you'll primarily deal with investment expense ratios. Specialized providers like MySolo401k.net might charge a setup fee (e.g., $300-$500) and an annual maintenance fee (e.g., $100-$200), but they offer more advanced features like checkbook control for alternative investments.

Traditional 401k and Safe Harbor 401k for Small Businesses

Now, let's talk about the big guns: the Traditional 401(k) and its cousin, the Safe Harbor 401(k). These are the most comprehensive retirement plans and are suitable for businesses with multiple employees, especially as you grow beyond the 100-employee limit of a SIMPLE IRA. While more complex, they offer the highest contribution limits and the most flexibility in plan design.

Traditional 401k Features and Compliance Considerations

- Who it's for: Businesses of all sizes, from small to large, with multiple employees.

- Contributions: Employees can contribute up to $23,000 for 2024 ($30,500 if age 50 or older). Employers can make matching contributions or profit-sharing contributions. The combined total (employee + employer) cannot exceed $69,000 for 2024 ($76,500 if age 50 or older).

- Roth Option: Most 401(k)s offer a Roth option for employee contributions.

- Loan Feature: Loans are typically available from 401(k) plans.

- Vesting: Employer contributions can be subject to a vesting schedule (e.g., 3-year cliff or 6-year graded vesting).

- Compliance: Requires annual IRS Form 5500 filing and adherence to complex non-discrimination testing rules (ADP/ACP tests) to ensure the plan doesn't disproportionately benefit highly compensated employees.

Safe Harbor 401k Simplifying Compliance for Employers

The Safe Harbor 401(k) is a variation of the Traditional 401(k) designed to simplify compliance. By meeting certain employer contribution requirements, you can automatically satisfy the non-discrimination testing rules, which can be a huge relief for business owners.

- Employer Contribution Requirements: You must either make a 3% non-elective contribution for all eligible employees (regardless of whether they contribute) or match employee contributions dollar-for-dollar up to 3% of compensation, and then 50% of the next 2% of compensation (totaling 4% match).

- Immediate Vesting: Safe Harbor contributions are immediately 100% vested.

- Benefit: Eliminates the need for complex non-discrimination testing, reducing administrative burden and ensuring highly compensated employees can maximize their contributions.

Traditional and Safe Harbor 401k Use Cases and Scenarios

If your business is growing and you have a significant number of employees, a 401(k) is the gold standard. A Traditional 401(k) offers maximum flexibility in plan design, but the non-discrimination testing can be a headache. If you're willing to commit to specific employer contributions, a Safe Harbor 401(k) can be a fantastic way to offer a robust plan without the compliance worries. For example, a tech startup with 20 employees looking to attract top talent might opt for a Safe Harbor 401(k) with a generous employer match.

Recommended 401k Providers and Pricing

401(k) plans involve more administrative services, so providers often charge setup fees, annual administration fees, and per-participant fees, in addition to investment fees.

- Guideline: Known for its affordable, transparent pricing and automated administration. They offer both Traditional and Safe Harbor 401(k)s.

- Human Interest: Another popular choice for small businesses, offering low-cost plans with a focus on ease of use and employee education.

- Fidelity: Offers comprehensive 401(k) solutions for businesses of all sizes, with a wide range of investment options and robust support.

- Vanguard: Provides cost-effective 401(k) plans, especially for those who prefer passive investing strategies.

Pricing: This is where it gets a bit more complex. Expect a setup fee (e.g., $500-$2,000), a monthly base fee (e.g., $50-$200), and a per-participant monthly fee (e.g., $5-$15 per employee). Investment expense ratios will also apply. For example, Guideline's Starter plan might be $39/month base fee + $8/participant/month, plus investment fees. Human Interest might offer similar pricing structures. Larger providers like Fidelity might have more customized pricing based on the size and complexity of your plan.

Comparing Retirement Plan Options Side by Side

Let's put it all together in a quick comparison to help you visualize the differences.

Key Differences SEP IRA vs SIMPLE IRA vs Solo 401k vs Traditional 401k

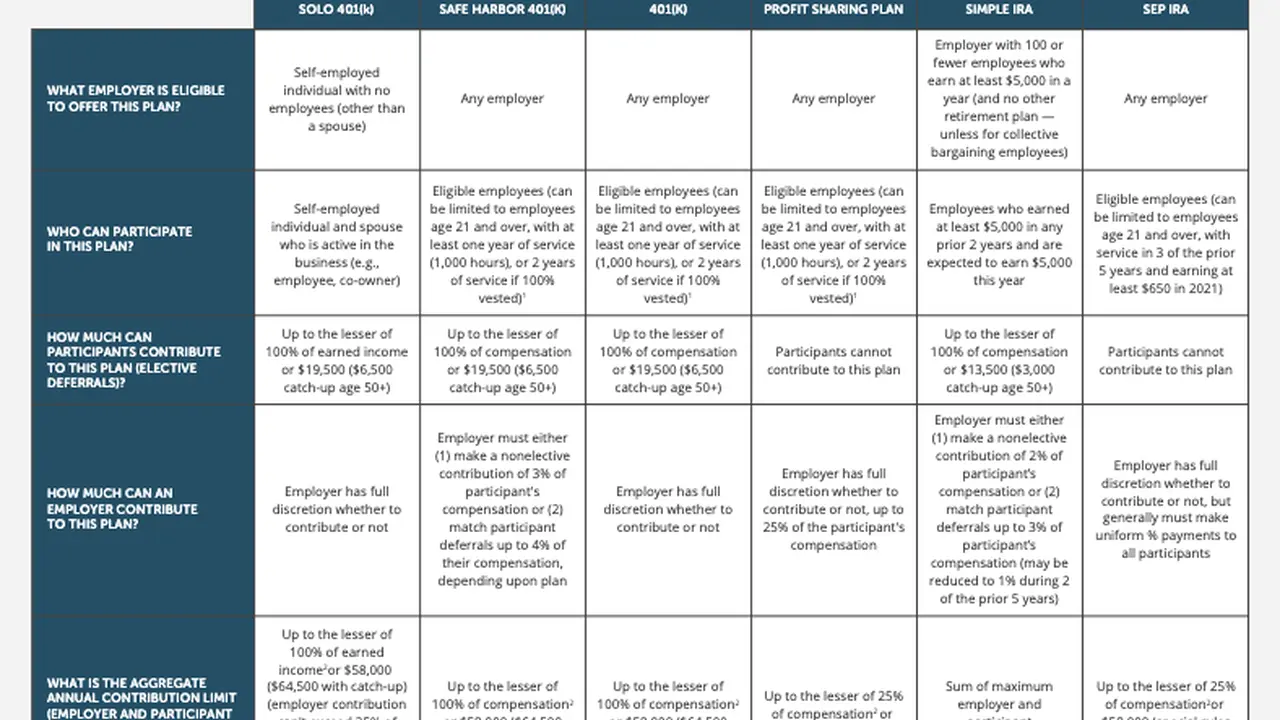

| Feature | SEP IRA | SIMPLE IRA | Solo 401(k) | Traditional/Safe Harbor 401(k) |

|---|---|---|---|---|

| Who it's for | Self-employed, few employees | 1-100 employees | Self-employed, no non-spouse employees | Any size business, multiple employees |

| Employee Contributions | No | Yes | Yes (as employee) | Yes |

| Employer Contributions | Yes (discretionary) | Yes (mandatory match or non-elective) | Yes (as employer) | Yes (discretionary or mandatory for Safe Harbor) |

| Max Total Contribution (2024) | $69,000 | $16,000 (employee) + employer match/2% | $69,000 | $69,000 |

| Roth Option | No | No | Yes (for employee contributions) | Yes (for employee contributions) |

| Loans Allowed | No | No | Yes (some plans) | Yes |

| Vesting | Immediate | Immediate | Immediate | Can be subject to schedule (Traditional), Immediate (Safe Harbor) |

| Administrative Complexity | Very Low | Low | Low (until $250k assets) | High (Traditional), Moderate (Safe Harbor) |

| Annual IRS Filing (Form 5500) | No | No | Yes (if assets > $250k) | Yes |

Choosing the Right Retirement Plan for Your Business

Alright, you've got the rundown on the main options. Now, how do you pick the best one for your unique situation? Here are some questions to ask yourself:

Factors to Consider Employee Count and Budget

- How many employees do you have? If it's just you (and maybe your spouse), a Solo 401(k) or SEP IRA is likely your best bet. If you have a few employees (under 100), a SIMPLE IRA is a strong contender. For more employees, a Traditional or Safe Harbor 401(k) becomes more appropriate.

- What's your budget for employer contributions? SEP IRAs and Traditional 401(k)s offer discretionary contributions, meaning you don't have to contribute every year. SIMPLE IRAs and Safe Harbor 401(k)s require mandatory employer contributions, which can be a significant cost but also a great employee benefit.

- How much administrative burden are you willing to take on? SEP IRAs are the simplest. SIMPLE IRAs are a bit more involved. 401(k)s, especially Traditional ones, require the most administrative effort and compliance.

- How much do you and your employees want to contribute? If maximizing your own contributions is a top priority, a Solo 401(k) offers the highest limits for self-employed individuals. For employees, 401(k)s generally allow for higher contributions than SIMPLE IRAs.

- Do you want to offer a Roth option? If you or your employees prefer tax-free withdrawals in retirement, a Solo 401(k) or a Traditional/Safe Harbor 401(k) with a Roth option is essential.

Making an Informed Decision for Your Financial Future

Don't feel like you have to figure this all out on your own. It's a big decision with long-term implications. Consider consulting with a financial advisor or a retirement plan specialist. They can help you analyze your specific business situation, employee demographics, and financial goals to recommend the most suitable plan. They can also help you navigate the setup process and ongoing compliance requirements.

Remember, offering a retirement plan isn't just about checking a box; it's about investing in your future and the future of your team. A well-chosen plan can provide significant tax benefits, help you attract and retain valuable employees, and ultimately contribute to the long-term success and stability of your small business. So, take the time, do your research, and make a choice that sets you up for a comfortable retirement and a thriving business!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)