Top 3 Tax Planning Strategies for US Small Businesses

Explore the 3 most effective tax planning strategies that US small businesses can use to minimize liabilities and maximize savings.

Explore the 3 most effective tax planning strategies that US small businesses can use to minimize liabilities and maximize savings.

Top 3 Tax Planning Strategies for US Small Businesses

Hey there, fellow small business owners! Navigating the world of taxes can feel like a maze, especially here in the US. But don't sweat it too much. With a bit of smart planning, you can significantly reduce your tax liabilities and keep more of your hard-earned money in your business. We're going to dive deep into three super effective tax planning strategies that every US small business should consider. We'll talk about specific products, how they fit into different scenarios, compare some options, and even touch on pricing. Let's get started!

Strategy 1 Maximizing Deductions and Credits for Small Business Tax Savings

One of the most straightforward ways to lower your tax bill is by maximizing your deductions and credits. Think of deductions as ways to reduce your taxable income, and credits as direct reductions of the tax you owe. It's like finding money you didn't even know you had!

Understanding Common Business Deductions for US Small Businesses

The IRS allows small businesses to deduct a wide range of expenses. Knowing what you can deduct is half the battle. Here are some common ones:

- Operating Expenses: This is a big one. It includes things like rent, utilities, office supplies, advertising, and professional services (accountants, lawyers). Keep meticulous records of all these.

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you might qualify. There are two methods: the simplified option (a standard deduction per square foot) or the regular method (deducting actual expenses like a portion of mortgage interest, utilities, and insurance).

- Vehicle Expenses: If you use your car for business, you can deduct actual expenses (gas, oil, repairs, insurance, depreciation) or use the standard mileage rate. Often, the standard mileage rate is simpler and can be quite generous.

- Business Travel, Meals, and Entertainment: Travel expenses for business are generally 100% deductible. For meals, it's usually 50% deductible if directly related to business. Entertainment expenses are generally no longer deductible, so be careful there.

- Employee Compensation and Benefits: Salaries, wages, bonuses, and benefits like health insurance premiums and retirement plan contributions are all deductible.

- Insurance Premiums: Health, liability, and other business insurance premiums are typically deductible.

- Interest Expense: Interest paid on business loans or credit cards is deductible.

- Depreciation: For assets like equipment, vehicles, and buildings, you can deduct a portion of their cost over their useful life. Section 179 deduction and bonus depreciation allow you to deduct a significant portion, or even the full cost, in the year of purchase for many assets.

Leveraging Tax Credits for US Small Business Growth

Tax credits are even better than deductions because they directly reduce your tax liability dollar-for-dollar. While deductions reduce your taxable income, credits reduce the actual tax you owe. Some common credits for small businesses include:

- Research and Development (R&D) Tax Credit: If your business is involved in developing new products, processes, or software, you might qualify for this credit. It's not just for big tech companies; many small businesses doing innovative work can claim it.

- Work Opportunity Tax Credit (WOTC): This credit encourages employers to hire individuals from certain target groups who face significant barriers to employment.

- Small Business Health Care Tax Credit: If you provide health insurance to your employees and meet certain criteria, you could be eligible for this credit.

- Energy-Efficient Commercial Buildings Deduction (179D): If you invest in energy-efficient improvements to your commercial building, you might qualify for this deduction.

Tools for Tracking Deductions and Credits for Small Business Owners

To maximize these, you need excellent record-keeping. Here are some tools that can help:

QuickBooks Online for Comprehensive Financial Management

Use Case: QuickBooks Online is a fantastic all-in-one solution for small businesses. It helps you track income and expenses, categorize transactions, generate financial reports, and even manage payroll. Its robust reporting features make it easy to identify potential deductions.

Comparison: Compared to manual spreadsheets or less integrated software, QuickBooks offers a more automated and comprehensive approach. It integrates with many banks and credit cards, pulling in transactions automatically.

Pricing: Plans typically range from about $30 to $200 per month, depending on the features you need (Simple Start, Essentials, Plus, Advanced). They often have promotional discounts for new users.

FreshBooks for Service-Based Business Expense Tracking

Use Case: FreshBooks is particularly strong for service-based businesses and freelancers. It excels at invoicing, time tracking, and expense management. Its intuitive interface makes it easy to snap photos of receipts and categorize expenses on the go.

Comparison: While QuickBooks is more comprehensive for inventory and complex accounting, FreshBooks is often praised for its user-friendliness and focus on invoicing and expense tracking, making it ideal for solo entrepreneurs or very small teams.

Pricing: Plans range from around $17 to $55 per month, with custom pricing for larger teams. They also offer a free trial.

Expensify for Automated Expense Reporting and Receipt Management

Use Case: Expensify is a dedicated expense management tool that automates receipt scanning and expense reporting. It's great for businesses with employees who incur many expenses, simplifying the reimbursement process and ensuring all deductible expenses are captured.

Comparison: Unlike full accounting software, Expensify focuses solely on expenses. It integrates well with other accounting platforms like QuickBooks and Xero, acting as a specialized add-on for expense management.

Pricing: Free for individuals, with team plans starting around $5 per active user per month.

Strategy 2 Strategic Entity Selection and Retirement Planning for Tax Efficiency

The legal structure of your business and how you plan for retirement can have a massive impact on your tax bill. Choosing the right entity and setting up smart retirement plans are crucial long-term tax strategies.

Choosing the Right Business Entity for US Tax Advantages

Your business entity determines how your profits are taxed. Here's a quick rundown:

- Sole Proprietorship: Easiest to set up, but no legal separation between you and your business. Profits are taxed on your personal income tax return (Schedule C). You're also subject to self-employment taxes (Social Security and Medicare).

- Partnership: Similar to a sole proprietorship but with two or more owners. Profits pass through to partners' personal returns. Also subject to self-employment taxes.

- LLC (Limited Liability Company): Offers personal liability protection. By default, an LLC is taxed as a sole proprietorship (if one owner) or a partnership (if multiple owners). However, an LLC can elect to be taxed as an S-Corp or a C-Corp, which can offer significant tax advantages.

- S-Corporation (S-Corp): This is where it gets interesting for many small businesses. An S-Corp allows profits and losses to be passed through directly to your personal income without being subject to corporate tax rates. The big advantage is that owners who work for the business can pay themselves a 'reasonable salary' (subject to payroll taxes) and then take the remaining profits as 'distributions,' which are not subject to self-employment taxes. This can lead to substantial savings.

- C-Corporation (C-Corp): A C-Corp is a separate legal entity and is taxed on its profits at the corporate level. Then, if profits are distributed to shareholders as dividends, those dividends are taxed again at the individual level (double taxation). While generally less favorable for small businesses due to double taxation, C-Corps can be attractive for businesses looking to raise significant capital or with plans for a public offering, as they can offer certain benefits like more flexible stock options.

When to consider an S-Corp election: If your business is consistently profitable and you're paying a significant amount in self-employment taxes as a sole proprietor or partner, electing S-Corp status for your LLC can be a game-changer. You'll need to pay yourself a reasonable salary, but the savings on self-employment taxes on the remaining distributions can be substantial. It's crucial to consult with a tax professional to determine if this is the right move for your specific situation.

Optimizing Retirement Plans for Small Business Owners and Employees

Setting up a retirement plan isn't just about saving for your future; it's also a powerful tax-saving tool. Contributions to many small business retirement plans are tax-deductible, and the money grows tax-deferred.

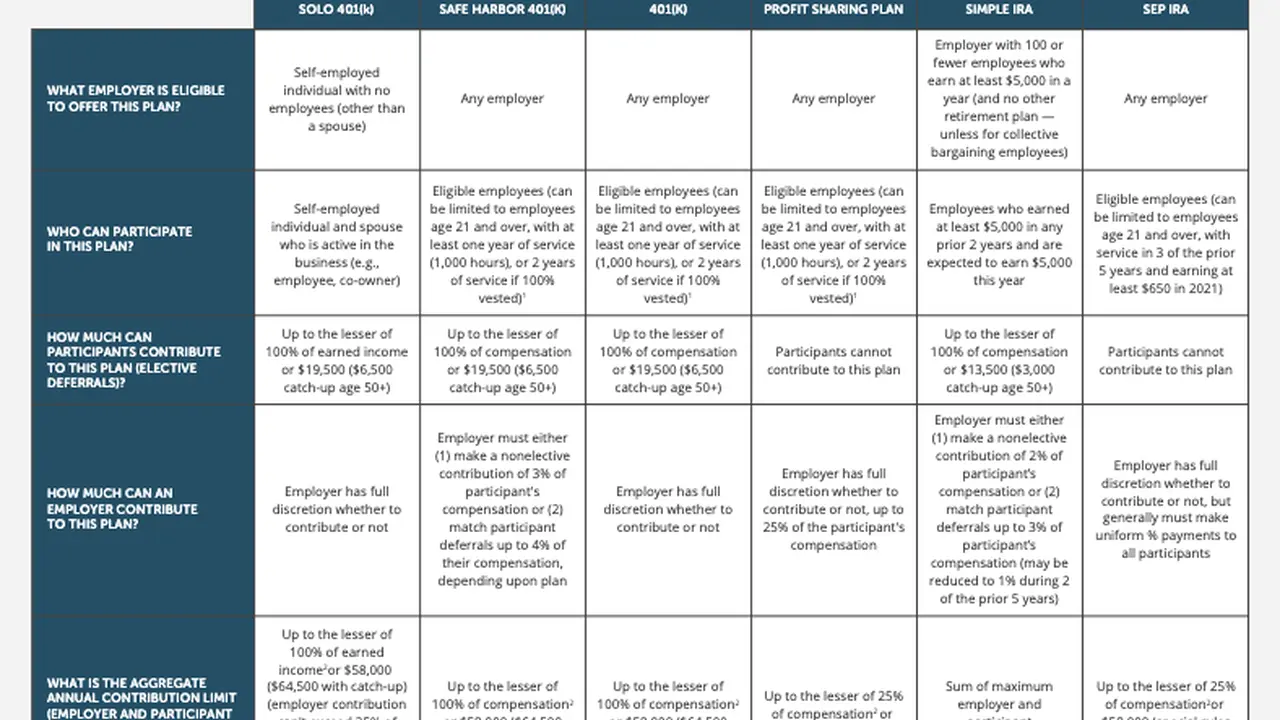

SEP IRA for Solo Entrepreneurs and Small Teams

Use Case: A Simplified Employee Pension (SEP) IRA is excellent for self-employed individuals and small business owners with few or no employees. It's easy to set up and administer, and you can contribute a significant portion of your income (up to 25% of compensation, or $69,000 for 2024, whichever is less).

Comparison: Simpler than a 401(k), with higher contribution limits than a traditional IRA. However, if you have employees, you must contribute the same percentage of compensation for them as you do for yourself.

Pricing: Generally no setup or annual fees for the plan itself, though investment fees apply to the underlying investments.

SIMPLE IRA for Small Businesses with Employees

Use Case: A Savings Incentive Match Plan for Employees (SIMPLE) IRA is a good option for small businesses with 100 or fewer employees. It's relatively easy to administer compared to a 401(k) and allows both employer and employee contributions.

Comparison: More flexible than a SEP IRA if you want employees to contribute, and generally lower administrative costs than a full 401(k). Employer contributions are mandatory (either a 2% non-elective contribution or a dollar-for-dollar match up to 3% of compensation).

Pricing: Low administrative costs, often just investment fees.

Solo 401(k) for Self-Employed Individuals with High Income

Use Case: If you're self-employed with no employees (other than your spouse, if they also work in the business), a Solo 401(k) offers the highest contribution limits. You can contribute as both an employee (up to $23,000 in 2024, plus catch-up contributions if over 50) and an employer (up to 25% of your net self-employment earnings), with a combined limit of $69,000 for 2024.

Comparison: Offers significantly higher contribution limits than a SEP or SIMPLE IRA, allowing for greater tax deferral. More administrative complexity than a SEP IRA, but less than a traditional 401(k) for businesses with employees.

Pricing: Can have some setup and annual fees, but many brokerage firms offer them with minimal costs.

Guideline for Automated 401(k) Management for Growing Businesses

Use Case: As your business grows and you have more employees, a traditional 401(k) might become the best option. Guideline offers automated 401(k) plans that are easy to set up and manage, making it accessible for small and medium-sized businesses.

Comparison: Guideline simplifies the often complex administration of 401(k) plans, offering a more affordable and user-friendly alternative to traditional 401(k) providers that might cater more to larger corporations.

Pricing: Starts around $39 per month plus $8 per participant per month, making it very competitive for small businesses.

Strategy 3 Proactive Tax Planning and Professional Guidance for US Small Businesses

The best tax strategy isn't a one-time event; it's an ongoing process. Proactive planning throughout the year and getting expert advice are key to long-term tax efficiency.

Importance of Year-Round Tax Planning for Small Business Success

Don't wait until April 14th to think about your taxes! Year-round planning allows you to make strategic decisions that impact your tax liability. This includes:

- Regular Financial Reviews: Periodically review your income and expenses to project your tax liability. This helps you identify opportunities for deductions or adjustments.

- Estimated Tax Payments: As a small business owner, you're generally required to pay estimated taxes quarterly. Underpaying can lead to penalties, so accurate estimation is crucial.

- Asset Purchases: Plan major asset purchases (equipment, vehicles) strategically. Buying them towards the end of the year might allow you to take advantage of Section 179 or bonus depreciation for the current tax year.

- Inventory Management: If you hold inventory, consider strategies like LIFO (Last-In, First-Out) or FIFO (First-In, First-Out) accounting methods, which can impact your cost of goods sold and, consequently, your taxable income.

- Charitable Contributions: Plan any charitable giving strategically. Business contributions can be deductible.

- Tax Loss Harvesting: If you have investments outside your business, consider selling losing investments to offset capital gains and potentially a limited amount of ordinary income.

Leveraging Professional Tax Advice for Optimal Outcomes

While DIY tax software is great for simple returns, small business taxes can get complex. A good tax professional is an invaluable asset.

Hiring a Certified Public Accountant (CPA) for Comprehensive Tax Services

Use Case: A CPA can provide comprehensive tax planning, preparation, and advisory services. They can help you choose the right business entity, identify all eligible deductions and credits, navigate complex tax laws, and represent you in case of an audit. They're essential for businesses with growing complexity or significant revenue.

Comparison: CPAs have extensive training and are licensed, offering a higher level of expertise and accountability than a general tax preparer. They can offer strategic advice beyond just filing your return.

Pricing: Fees vary widely based on location, complexity of your business, and services provided. Expect to pay anywhere from a few hundred dollars for a simple business return to several thousands for ongoing advisory and complex filings. Many CPAs offer hourly rates (e.g., $150-$400/hour) or flat fees for specific services.

Utilizing Tax Software with Professional Support for Hybrid Approach

Use Case: For businesses with relatively straightforward tax situations, using tax software like TurboTax Business or H&R Block Premium can be a cost-effective solution. Many of these platforms now offer options to connect with a tax professional for review or advice.

Comparison: More affordable than a full-service CPA, but requires you to do more of the data entry and initial understanding. The professional support option provides a safety net.

Pricing: Software typically costs $100-$200 for the business version. Adding professional review or advice can add another $100-$500, depending on the service level.

- TurboTax Business: Great for S-Corps, C-Corps, Partnerships, and multi-member LLCs. User-friendly interface guides you through the process.

- H&R Block Premium & Business: Offers similar features to TurboTax, often with competitive pricing and good support options.

Engaging a Tax Attorney for Complex Legal and Tax Issues

Use Case: If your business faces complex legal and tax issues, such as mergers and acquisitions, international tax implications, or serious IRS disputes, a tax attorney is the specialist you need. They combine legal expertise with tax knowledge.

Comparison: While CPAs focus on compliance and planning, tax attorneys specialize in the legal aspects of taxation, offering representation and advice on highly intricate matters.

Pricing: Tax attorneys typically charge higher hourly rates, often ranging from $250 to $800+ per hour, depending on their experience and the complexity of the case.

Implementing Tax-Advantaged Business Practices for Long-Term Savings

Beyond specific deductions and entity choices, adopting certain business practices can inherently lead to tax advantages:

- Automate Record Keeping: Use accounting software or dedicated expense trackers to ensure every deductible expense is captured.

- Regularly Review Financial Statements: Understand your profit and loss, balance sheet, and cash flow statements. These provide insights into your business's financial health and potential tax implications.

- Stay Updated on Tax Law Changes: Tax laws change frequently. Subscribing to tax news, attending webinars, or having a proactive CPA can keep you informed.

- Consider State and Local Taxes: Don't forget about state and local taxes, which can vary significantly. Your tax professional can help you navigate these as well.

- Plan for Estimated Taxes: Avoid penalties by accurately estimating and paying your quarterly taxes.

- Document Everything: The golden rule of taxes: if it's not documented, it didn't happen. Keep receipts, invoices, contracts, and all relevant financial records organized.

By actively engaging in these three strategies – maximizing deductions and credits, making smart entity and retirement plan choices, and committing to proactive planning with professional guidance – your US small business can significantly reduce its tax burden. It's all about being informed and making strategic decisions throughout the year, not just when tax season rolls around. Happy saving!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)